In a nutshell

This first half-year was marked by the resilience of credit markets. Markets were dominated by developments in the Middle East conflict and the rise of AI. As after last year’s US tariff shock, the market quickly digested the Iranian conflict. Credit spreads have today returned to their pre-conflict levels. Investors viewed the conflict’s impact as an inflationary and interest-rate shock. However, recession fears remained very contained. Government bond yields rose across the curve, particularly at the short end. Investors notably reassessed inflation risks, expectations for the path of monetary policy, and questioned the trajectory of public deficits.

Indeed, the economic backdrop remained supportive despite persistent geopolitical uncertainties. Growth and inflation forecasts were revised because of the conflict, but the probability of a recession scenario fell sharply after the ceasefire announcement at the end of March. Concerns had focused on massive destruction of regional infrastructure and oil prices remaining very high for a prolonged period. In mid-June, the signing of a memorandum of understanding between Washington and Tehran initially pushed oil prices down. But the truce proved fragile: new strikes near the Strait of Hormuz pushed oil prices back up, with Brent reaching $85 per barrel. This volatility is likely to persist as long as tensions continue.

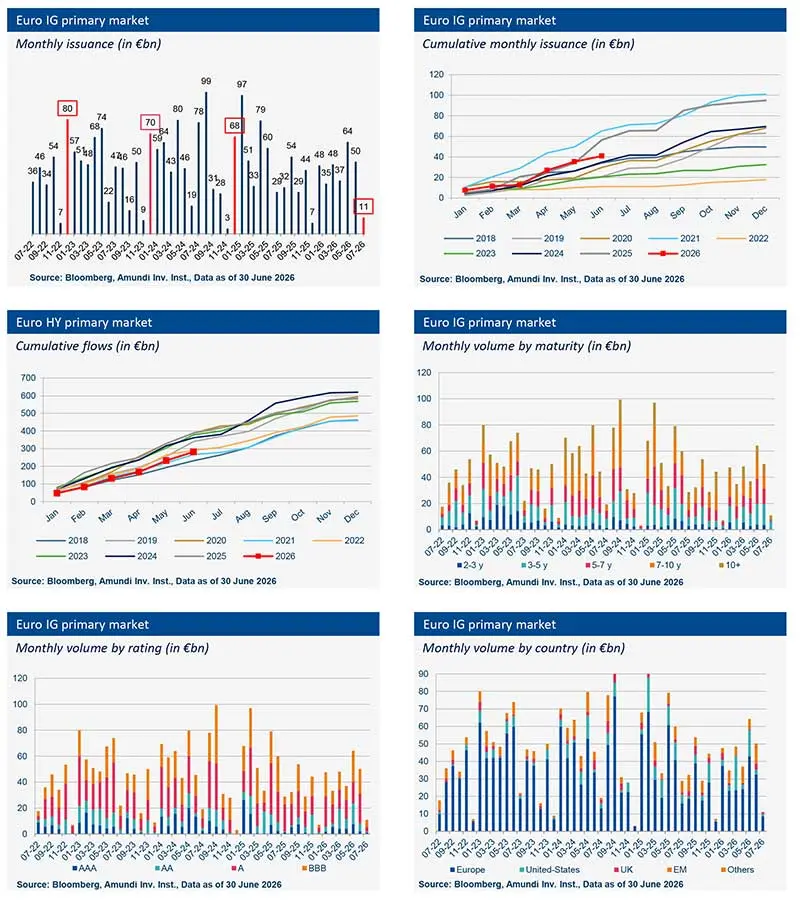

In this context, the primary market remained particularly active. The euro-denominated corporate debt primary market recorded a very dynamic first half, driven by US issuers and sustained investor demand. The period was marked by a surge of AI-related bonds. These issuances helped produce a record volume of bonds from US issuers, attracted by favorable financing conditions and the depth of the euro market. Utilities also contributed substantially to the rise in volumes. M&A was a second driver.

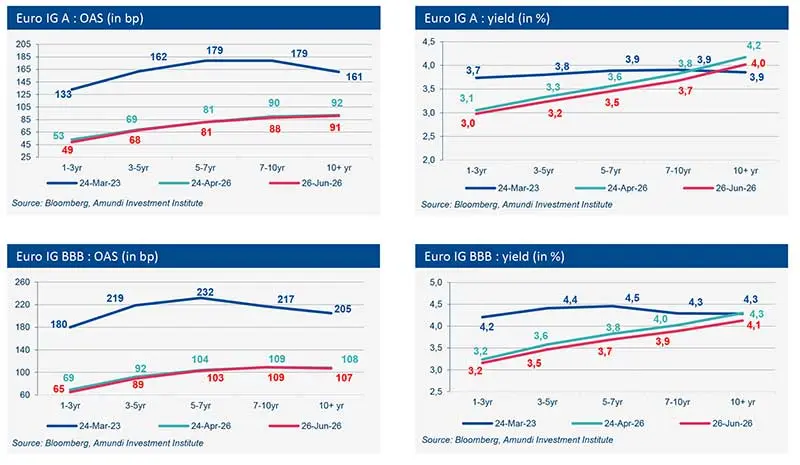

Investor demand has consistently been present. Spreads have returned to their pre-conflict historic lows, but higher rates have improved offered yields. Attractive yield levels continue to draw flows despite tighter spreads. We expect market activity to recover quickly from the end of August, driven by AI-related needs and continued M&A. August is traditionally a month when primary market activity slows.

Primary market Investment Grade

Market data

Get to know our treasury offering