Summary

Highlights

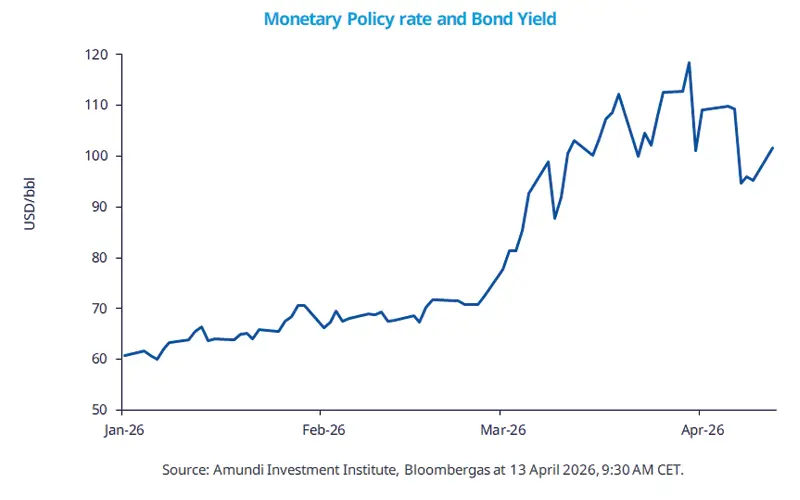

An uncertain and volatile environment around US-Iran negotiations is affecting oil prices. Any sign of subsiding war risks would obviously be positive for the markets.

What matters most for the economy is the flow of shipping traffic through the Strait of Hormuz.

We think investors should avoid being carried away by excessive euphoria and stay focused on long-term convictions and diversification*.

In this edition

News flow relating to the Middle East crisis highlights how rapid progress — or derailment — in talks can quickly alter market sentiment. Initially, hopes that traffic through the Strait of Hormuz might reopen allowed oil prices to fall amid expectations of a resumption in supply. At the same time, a relief rally was seen across US, European and emerging-market equities. While the temporary ceasefire between the US and Iran was the obvious catalyst, the reality on the ground — particularly whether traffic through the Strait has returned to normal — may be different. This was also evident from the failure of the weekend talks between the US and Iran, which caused an expected spike in oil prices. We believe that if oil stabilises at lower levels, this would, of course, be positive for the economy. But the big question is how quickly energy production — not just oil — can return to normal levels, and this remains uncertain. As a result, it is unlikely that oil prices will settle close to pre-war levels in the near term.

* Diversification does not guarantee a profit or protect against a loss

Key dates

US small business optimism, PPI |

EZ industrial production, US Fed beige book |

China GDP, UK Industrial production |

Read more