Summary

Highlights

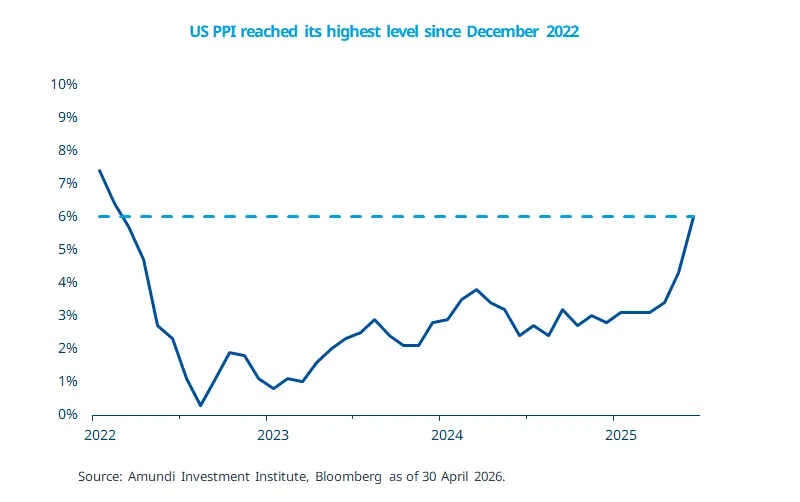

US input price inflation accelerated in April, coming in significantly above market expectations.

Bond yields, particularly short-dated ones, are moving higher owing to higher near-term inflation expectations. Additionally, a recent auction of 30-year USTs was completed at yields close to 5%, for the first time since 2007.

- We think the Fed would like to balance the need to control inflation with any potential fragilities in the economy.

In this edition

US PPI, a measure of inflation at the producer level, rose to 6% year on year in April, the highest since December 2022 and well above market expectations. Energy price inflation also rose sharply since March. The data suggest that the war in the Middle East is beginning to feed into the real economy through higher input costs for companies, raising the risk that these costs may be passed on to consumers. In markets, 2-year Treasury yields, which are highly sensitive to inflation and monetary policy expectations, have moved above 4.0% — their highest level since June 2025 — on concerns about price pressures. We believe the key driver will be how long energy prices remain elevated, which in turn depends on the duration of the conflict and disruptions through the Strait of Hormuz. On monetary policy, we expect the Fed to remain in wait-and-see mode this year, although some FOMC members are becoming alert to inflation risks. While we believe the new Fed Chair, Kevin Warsh, may take a reasonably balanced, wait-and-see approach, we are monitoring any potential political pressure on the central bank.

Key dates

19 May Japan GDP 1Q, UK unemployment rate, South Africa CPI |

20 May Eurozone CPI. UK CPI and PPI, FOMC Minutes |

22 May Japan CPI, Germany IFO, US University of Michigan Consumer confidence |

Read more