Summary

Highlights

Global equities closed their best quarter since late 2020. Emerging markets remain the strongest- performing area, posting their best quarter since 2009.

Technology and AI-related themes remained the main drivers, but momentum faded in June as investors rotated within the AI-trade and across sectors and geographies.

Looking ahead, we expect greater investor scrutiny and a broader push towards diversification. Selectivity and fundamentals should remain key.

In this edition

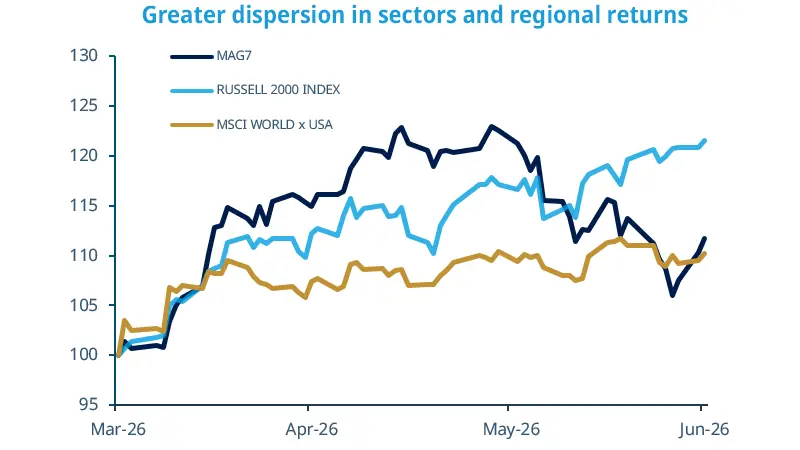

Global equities extended their gains last quarter, shrugging off geopolitical risks, shifting expectations for central bank policy and volatile sentiment around the AI trade. The broadening away from crowded trades is a key market theme set to continue. In the US, performance widened as investors rotated out of the so called Magnificent 7 into industrials and defensives, while small caps (Russell 2000 Index) outperformed on the back of resilient growth, employment and consumer spending, which support domestic corporate profits. The same pattern has emerged across regions. European equities outperformed into quarter-end as investors sought to reduce concentration risks and broaden exposure to themes that should benefit from a more investment-led model of growth and a German fiscal push. Other laggard areas, such as emerging markets beyond Asia tech, could benefit from this rotation, offering opportunities also across the entire AI value chain; Latin America is particularly well placed thanks to demand for AI-related raw materials.

Key dates

6 Jul EZ Sentix Investor Confidence, PPI and Retail sales; US ISM Services |

8 Jul US FOMC Meeting Minutes |

9 Jul China PPI and CPI, Mexico CPI |

Read more